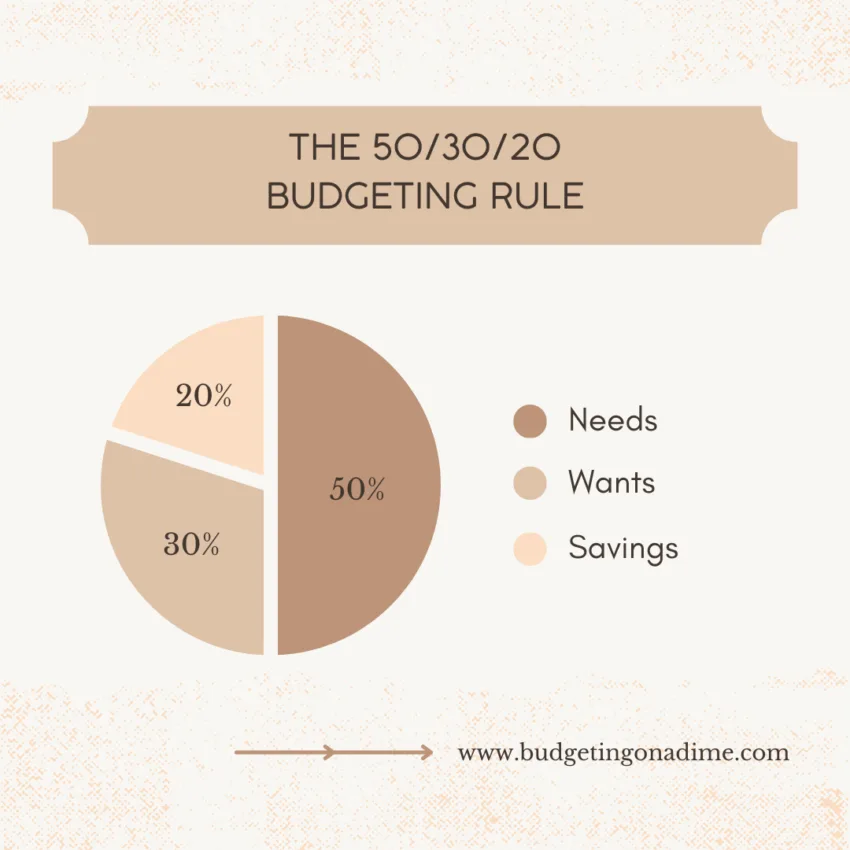

The 50/30/20 rule is simple enough. It divides your post-tax income into three key spending areas: 50% for necessities, 30% for personal wants, and 20% for building savings and reducing debt.

Historical Context of the 50/30/20 Rule

The 50/30/20 budgeting rule has been around for a while, but its origins may surprise you. This simple guideline for dividing your income was popularized by Senator Elizabeth Warren back in the 2000s, but the concept has much deeper roots.

The idea of allocating your money into broad categories like “needs,” “wants,” and “savings” has been around for decades. Personal finance experts have long advised people to be mindful of balancing these three areas. However, the specific 50/30/20 breakdown emerged as a rule of thumb that was easy for the average person to remember and apply.

The 3 Categories of the 50/30/20 Rule Explained

Essential Expenses (50%): This covers the non-negotiable costs of living – things like rent/mortgage, utilities, groceries, and transportation. These are the expenses you simply can’t avoid.

Discretionary Spending (30%): This is the fun part of your budget – money allocated for dining out, entertainment, hobbies, and other lifestyle choices. It’s important to be mindful, but you should still leave room to enjoy yourself.

Savings and Debt Payments (20%): The final 20% should go towards building up your savings and paying down any outstanding debts. This helps you achieve long-term financial stability and security.

Essentials for the 50% Needs Category

The 50% Needs Category in the 50/30/20 budgeting rule is often the most straightforward to define, but people can still get stuck on this. Let’s look in-depth at what counts as true “needs” in this budget.

Rent, utilities, groceries, transportation – these are the no-brainers. The essentials you absolutely can’t live without. But what about things like the internet, cell phone, or streaming services? If you work from home or have kids, they may be necessities. They can fall into a grayer area, but it will be up to your unique circumstances whether or not they are included.

The key is to look at your circumstances and determine what you truly need to function and cover your basic quality of life. Pare down to only the necessities and leave the “wants” for the 30% discretionary spending. It may require some tough choices, but staying focused on true needs is crucial for making the 50/30/20 budget work.

Remember, the 50% Needs are the foundation. Be ruthless in this category, and the rest of your budget will be that much easier to manage.

Allocating the 30% Wants Category

This is the fun part of the 50/30/20 rule (as fun as budgeting can be), but it’s easy to let it get out of hand if you’re not careful.

First off, what even counts as a “want” in this scenario? Basically, anything that’s not a necessity or an investment. Eating out, entertainment, shopping sprees – those all fall under the “wants” umbrella. .

Now, allocating that 30% can be a balancing act. You don’t want to deprive yourself, but you also don’t want to blow it all in one place. Try to spread it out across different categories – a little for dining out, a little for that new gadget you’ve been eyeing, a little for a weekend getaway. That way, you’re satisfying various wants without going overboard.

Remember, the 50/30/20 rule is a guideline, not a rigid rule. If your “wants” end up being a bit more than 30%, don’t stress too much. The key is being mindful of your spending and making sure your essentials are covered first. As long as you’re keeping an eye on that discretionary budget, you’re on the right track.

Prioritizing the 20% Savings Category

Saving 20% of your income is no easy feat. It takes discipline, sacrifice, and a whole lot of commitment. But the 20% savings category is the key to building a solid financial foundation.

The 20% isn’t just money sitting in a bank account. It’s your ticket to a more secure future. Whether it’s saving for retirement, building an emergency fund, or investing in your dreams, that 20% is the backbone of your financial well-being.

It might mean cutting back on the occasional latte or saying no to that impulse buy. But it’s key for the long-term payoff. When life throws you a curveball, your savings will be there to cushion the blow.

How to Implement the 50/30/20 Rule for Your Finances

The 50/30/20 rule is a simple yet effective way to manage your finances, but implementing it can be trickier than it seems. Here’s a candid look at how to make the 50/30/20 rule work for you:

First, you must be brutally honest about your spending. Track every single expense for a month or two to get a clear picture of where your money is going. This will help you identify areas to cut back on discretionary spending so you can allocate more towards savings and debt repayment.

Next, make the tough choices. Cutting back on dining out, entertainment, and other “wants” is never fun, but it’s necessary to stick to the 50/30/20 guideline. Be prepared to make some lifestyle changes, at least temporarily, to get your finances on track.

Finally, make savings and debt repayment automatic. Set up recurring transfers to your savings account and make extra payments towards high-interest debt. The less mental effort required, the more likely you’ll be to follow through long-term.

The 50/30/20 rule works, but only if you’re willing to be honest with yourself and make some difficult decisions. It’s not easy, but taking control of your finances will pay off in the long run.

Pros and Cons of Following the 50/30/20 Budgeting Approach

The 50/30/20 budgeting rule is a popular personal finance strategy, but it’s not without its pros and cons.

On the plus side, the 50/30/20 rule provides a simple framework for allocating your income – 50% for necessities, 30% for discretionary spending, and 20% for savings. This can be a helpful guideline, especially for those new to budgeting. Or those who function best following rules.

However, the rigidity of the 50/30/20 split may not work for everyone. Your needs and priorities may not fit neatly into those percentages, leading to stress and frustration trying to make it work.

For example, freelancers whose income fluctuates may have a difficult time. Also people living in high-cost-of-living cities may also have a difficult time making necessities fit into 50% when rent may take up that entire category.

There are also alternative budgeting methods, like the zero-based budgeting method or the 60/20/20 rule, that may be a better fit depending on your financial situation and goals. The key is finding an approach that aligns with your unique circumstances.

At the end of the day, personal finance is personal. The 50/30/20 rule can be a solid starting point, but don’t be afraid to tweak it or explore other options to find what works best for you.

Final Thoughts: Should You Adopt the 50/30/20 Rule for Your Finances?

The 50/30/20 rule provides a simple, effective framework to help you master your money, but it is far from a one-size-fits-all method. Decide if this budgeting technique is right for you and take the first step towards better money management today.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

1 thought on “The 50/30/20 Rule: How To Easily Master the Basics”

Comments are closed.