There’s a lot of bad information out there, and it’s hard to understand credit scores. Let’s sift through some of the most common credit score myths and set the record straight on the top seven misconceptions that could be damaging your financial health. Many people are unwittingly making mistakes because they either don’t understand how a credit score is calculated or what actually matters. It’s time to separate fact from fiction and empower yourself with information—from the impact of checking your score too often to the role of payment history.

The Importance of Understanding Credit Score Myths

Understanding credit score myths is quite helpful in anyone’s quest to retain a healthy financial profile. Misinformation about how credit scores work can lead to some costly mistakes that might impact your capability to get loans, housing, or even employment opportunities. By debunking these myths and forming a clear, functional understanding of how credit scoring really works, you are empowering yourself to make good choices regarding your financial health.

A very common myth is the idea that you will lower your credit score by checking your credit score. Actually, your rating isn’t hurt at all when you monitor your score with soft inquiries, like from credit monitoring services. The key here is to realize the difference between soft and hard inquiries. Whereas the hard inquiries from loan applications themselves tend to drop your score, personal access to your credit score does nothing to hurt it. This knowledge will empower you in keeping track of your financial health without any apprehension.

Believing Credit Score Myths Can Lead to Costly Financial Mistakes

Most people don’t realize how much a credit score influences their financial stability. It tends to reflect your credit history and reflects your responsibility with debt. If a person neglects this important part of personal finance, then that person might suffer serious economic detriment.

The first myth concerns credit card balances and how the balance will influence your credit score. People generally believe that keeping a balance on credit cards is good to keep your score boosted, but really high balances can hurt your credit utilization ratio. That is the amount of credit in use compared with the total amount of credit available to you, and high balances signal financial instability to the lenders. It is very important to keep this low by attempting to pay off all the balance every month.

Probably another widespread myth is that carrying a credit card balance will help improve your score. On the other hand, understanding a credit utilization ratio really shows that high balances actually can hurt your rating by increasing the ratio. Low balances coupled with effective management are what constitutes a healthy credit profile. Knowing how payment history impacts your score underlines the significance of timely payments and responsible behavior of debt handling as ways of maintaining or improving your rating over time.

Another common factor most people get wrong is how important payment history is to your credit score. Your payment history leads the way in the determination of your credit score because it shows the lenders your reputation for making timely payments. One missed payment can have a diminishing impact and reduce your credit score. Monitoring this aspect regularly through tools such as Credit Karma will keep you in step with the payments and keep your credit history length in good books.

Besides this, having muddled types of debt—credit card debt versus installment loans—all leads to poor financial decisions. Both types of debt affect your general financial health, but each bears differently on your credit score. Mastering how each type of debt affects your score is critical to managing debt correctly and avoiding those pitfalls that can significantly imperil your financial stability in later life.

FICO 10: Separating Fact from Fiction in New Credit Scoring Models

With new models, like the FICO 10, breaking out, it is now more important than ever to be educated and know some of the myths flying around about credit scores. The newer models make changes and updates that could affect the way your credit score is calculated. Being able to understand these changes gives you a better foundation on which to make informed decisions when it comes to your credit health.

The Importance of Payment History in New Scoring Models

Another major factor is how these new scoring models view payment history. Your history with on-time payments is major in determining how creditworthy you are. Delinquent payments can ding your score, so paying bills on time is paramount. Credit monitoring services can help keep a tab on your payment history and warn you against impending trouble that has the potential to dent your score.

The Importance of Credit Utilization Ration

The other important factor that the new scoring model impacts is an understanding of credit utilization ratio. The credit utilization ratio, in simple terms, refers to the proportion of available credit that one is using at any given time.

Keeping this ratio low, preferably below 30%, shows the lenders that you use credit responsibly. The high balances raise this percentage and, correspondingly, lower your score. With knowledge, you can go ahead and work on this portion of your credit profile by keeping in mind just how much you charge, compared to the limits on your cards, which, with some time, may or could improve your score.

Another big factor that influences your credit score, according to updated modeling like FICO 10, comes from how long you’ve had credit. The longer your credit accounts have been open, the less risky you appear to lenders. That is because a more extensive history provides more information on which to base your financial behavior. So, if you close older accounts, you’re inadvertently shrinking that history and stand to decrease your score under these newer models. It should represent a balance found between managing the active accounts effectively and responsibly utilizing new credit, if necessary.

Credit Score Myth #1: Checking Your Credit Score Lowers It

Fact: Soft Inquiries Don’t Impact Your Credit Score

Now, let’s debunk the first credit score myth: checking your credit score lowers it. The reason so many people do not check their credit score is because they are dubious about seeing one’s financial standing hurt as a result of this, whereas, in reality, this myth couldn’t be more false. It will actually keep you ahead in monitoring your credit score through the facilities provided by either Credit Karma or Experian without any negative consequences.

There are two types of queries about credit scorings: soft and hard inquiries. Inquiries such as checking your score or getting pre-approved for a loan have no bearing at all on your credit score. These are routine checks that allow you to be in the know without any kind of repercussions. On the other hand, hard inquiries are those in which a lender accesses your credit report because you have applied for new credit on a certain credit card or a loan. Those types of inquiries do have the potential to hurt your score a bit, but only in the short run.

Being able to make out the difference between soft and hard inquiries is critical in case you want to manage your credit effectively. By monitoring your credit score with reliable services and keeping up with changing events regarding your report, you can head off any discrepancies or issues before they become problems. Remember, knowledge about your finances is power, and understanding the most current status of your credit makes for a very smart move toward longer-term financial stability.

Credit Score Myth #2: Carrying a Balance Helps Boost Your Credit Score

Fact: High Balances Increase Your Credit Utilization Ratio

A lot of people think that carrying a balance indicates you are using credit and helps your score. But in fact, it is the exact opposite. Credit card balances that are high in relation to your overall limit can hurt you by lowering the utilization ratio, an important component when it comes to what determines a good credit score. This is calculated as a ratio, where your total credit balance is divided by the sum limit across all your credit accounts. If this ratio gets too high, it can hurt your credit score with the major credit bureaus.

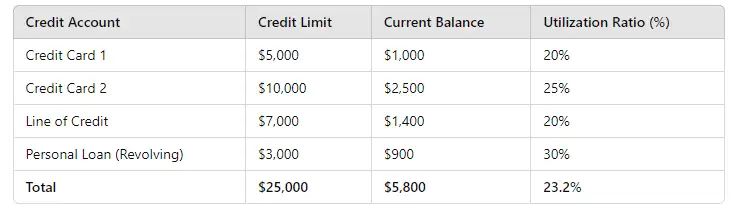

Credit Utilization Example

Credit Limit: This is the maximum amount of credit available on each account.

Current Balance: The outstanding balance currently owed on each credit account.

Utilization Ratio (%): Calculated as (Current Balance / Credit Limit) * 100 for each account.

Total Utilization Ratio: Calculated as the total current balance divided by the total credit limit, i.e., (Total Current Balance / Total Credit Limit) 100. In this example, it’s (5,800 / 25,000) 100 = 23.2%.

The Difference Between Credit Card Debt and Installment Loans

It’s important to understand the difference between credit card debt and installment loans, like student or car loans, and how they affect your score. Credit card debt directly influences your utilization ratio, and if you don’t keep it in check, it can quickly drag down your score. Installment loans, on the other hand, distribute the risk differently and are viewed in another way by lenders.

Paying off your credit cards in full every month and keeping your balances low not only helps you avoid penalties related to your utilization ratio but also builds good financial habits that can benefit many areas of your life.

Using Credit Monitoring Services to Track Your Utilization Ratio

Luckily credit monitoring services can help you keep an eye on your utilization ratio and overall credit health. You can regularly your balances and limits, and you can avoid maxing out your cards, which can hurt your score. A 30% utilization ratio (or below!) shows lenders you’re responsible for your credit.

Understanding how to manage high balances is key to maintaining or improving your credit score. While it might be tempting to let balances linger and pay them off slowly, this can actually harm your score over time. FICO 10 looks at how consistently you carry high balances, so it’s important to keep them low to show responsible credit usage.

Credit card debt impacts your score differently than installment loans, like student or auto loans, due to factors like payment history and overall debt load. Credit cards usually have higher interest rates, so managing those balances effectively is imperative (yes that sounds dramatic but paying back credit card interest is hard to recover from). By paying down high balances immediately and using tools like free credit monitoring services, you can set yourself up for financial success.

Credit Score Myth #3: Income Directly Impacts Credit Score

Fact: Credit Scores Do Not Consider Income, Only Credit Behavior

Your income level doesn’t directly affect your credit score. Whether you’re a high-earning executive or a student working part-time, what really matters to the credit bureaus are your financial habits.

They care more about how you manage your debts and bills than how much money you make each month. Paying your bills on time is one of the most important things you can do for your credit score. When you miss payments, it can seriously hurt your score, but consistently paying on time helps to boost it. It’s also important to keep your balances low and use credit wisely, as this shows you can handle debt responsibly.

Although your income affects your ability to pay off debts, it doesn’t directly influence your credit score. What matters more to lenders is that you’re making payments on time and keeping your credit usage low. This is why having a solid payment history and managing how much of your available credit you’re using is so important.

Concentrating on these aspects can help you make well-informed decisions to raise your credit score and secure your financial well-being in the long run.

Additional Info: How Higher Income Can Indirectly Improve Credit Limits

Earning a higher income can help you get approved for higher credit limits. When lenders assess your creditworthiness, they often consider your income to determine how much credit to extend. A higher income signals to lenders that you’re capable of repaying debts, which can result in higher limits on your credit cards or loans.

This can really help you keep your credit utilization in check. With a higher income and bigger credit limits, it’s easier to keep your balances low without using up too much of your available credit. Managing your credit this way can gradually boost your score over time.

Credit Score Myth #4: Closing Old Credit Cards Improves Your Score

Fact: Closing Cards Can Increase Your Utilization Ratio and Lower Average Account Age

A lot of people think that closing old credit cards will automatically improve their credit score, but it’s actually a bit more complicated. In reality, closing an old account can sometimes do more harm than good.

One of the main reasons is that it affects your credit utilization ratio—basically, how much of your total available credit you’re using. When you close a card, you’re cutting down the amount of credit you have to work with, which can make it seem like you’re using a larger portion of your available credit. This higher utilization can end up lowering your score.

You also need to consider how closing old cards affects the average age of your credit accounts. Your credit score benefits from having a longer credit history because it shows lenders that you’ve managed credit responsibly over time. If you close one of your oldest accounts, it could lower the average age of your credit history, which might not look as good to lenders.

So, before closing an old credit card, it’s important to consider how it might affect both your credit utilization and the length of your credit history.

Additional Info: Alternative Ways to Maintain Your Credit Accounts

While closing old credit cards may not always be beneficial for improving your score, there are alternative strategies you can consider to keep these accounts active without hurting your standing with creditors.

To keep old credit cards active, try using them for small recurring expenses, like a subscription service, and paying off the balance each month. This way, the account stays open, and you continue to build a solid payment history.

Currently, I have an old card with no bonus points that I only use to charge my $1.99 Hulu subscription each month. I’ve set it up for auto-payment, so I don’t even have to think about it, and it helps keep my credit history intact.

Another easy option is to set a reminder to use the card once in a while for small purchases. This way, it stays active without piling up debt or messing with my credit utilization.

Credit Score Myth #5: Paying Off Debt Always Increases Your Credit Score

Fact: Paying Off Installment Loans Might Temporarily Lower Scores

So, you’ve finally made your last student loan payment and keep refreshing your credit score, waiting for it to shoot through the roof, right? Well, I have some bad news for you… It’s not always that simple.

While paying off debts like student loans or auto loans is definitely a smart move, it’s not going to give your credit score the instant boost you might expect. In fact, you might even see a small dip at first. This happens because credit scoring models, like FICO 10, consider your overall credit history and behavior, not just whether you’ve paid off a loan.

Why Paying Off a Loan Might Cause a Temporary Dip in Your Score

One reason your score might drop a bit is due to something called your ‘credit mix. This refers to the variety of accounts you have, such as credit cards, car loans, or mortgages. When you pay off an installment loan, you’re left with fewer types of credit in your profile, which can slightly lower your score. But don’t worry—this is just temporary and shouldn’t discourage you from paying off debt.

Another factor is the average age of your accounts. Credit history length is an important part of your score, and the longer your accounts have been open, the better it is for your credit. When you pay off a loan and close the account, it can actually make your credit score dip a little bit because it lowers the average age of your accounts.

But here’s the good news: the most important things for your credit score are still paying your bills on time and keeping your credit card balances low. Learning these small details about how paying off debt affects your credit score can help you make better financial choices and stay calm.

So, even if your score takes a temporary hit after paying off a loan, it will all be okay. The long-term benefits of knocking out debt and improving your financial health definitely outweigh any short-term effects. Just keep an eye on your credit report with free monitoring tools to see how things change, and adjust your game plan as needed.

Credit Score Myth #6: My Employer Can See My Credit Score

Fact: Employers Can Only Access a Limited Version of Your Credit Report

A lot of people think their employers can access their credit score, but that’s not the case. Employers may check a specific part of your credit report when considering you for a job, but they won’t see your actual credit score. Instead, they’re usually looking at specific details in your credit history, like whether you have a lot of debt or if there are any signs of financial trouble.

It’s good to know that the information employers can see is pretty limited—they don’t get a full picture of your credit score or a detailed breakdown of it. What they’re really interested in is whether you manage your finances responsibly. For example, they might check if you’ve been handling your debts well or if any issues could raise concerns about your financial stability.

If you’re worried about how your credit history might affect job opportunities, it helps to understand what potential employers can actually see on your report. By knowing what information is available to them and how it could be viewed, you can take steps to address any concerns and make sure you present yourself in the best light. Just remember that while employers can review some aspects of your credit history, they don’t see the same level of detail that lenders or credit monitoring services do.

Legal Note: Consumer Protections Around Employment Credit Checks

When you’re applying for jobs, there are rules to protect you, especially when employers want to check your credit history. The Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) make sure companies follow fair practices through the Fair Credit Reporting Act (FCRA). This law ensures that employers can’t access your credit report without your knowledge—they need your written permission first.

If a potential employer checks your credit report and decides not to hire you because of what they find, they have to tell you. The law requires them to notify you, provide you with a copy of the report, and explain your rights. These measures help protect you from being unfairly judged based on your financial history. It helps to ensure the hiring process remains fair and transparent.

Fact: Defaulting on Student Loans Can Significantly Damage Scores

Let’s set the record straight: student loans absolutely impact your credit score. I know this from personal experience. How you handle your student loan payments matters—a lot. Your payment history is a major factor in determining your credit score, so if you miss a payment or default on your loans, it can really hurt your score.

If you’re finding it hard to keep up with payments, don’t ignore the problem (been there done that, it doesn’t work). Reach out to your lender and look into your options. Programs like income-driven repayment plans can help you manage payments without tanking your credit.

It’s also important to understand how different types of debt affect your credit score. Student loans are installment loans, meaning you borrow a fixed amount and pay it off over time. Paying these off shows responsible borrowing. But credit cards work differently; carrying a high balance increases your credit utilization ratio, which can drag your score down.

The truth is, managing debt takes some careful attention, whether it’s student loans or credit cards. Don’t fall for the myth that student loans won’t impact your credit—they absolutely do. That’s why it’s so important to stay on top of your payments. And if you’re struggling, don’t wait—reach out right away. There are people who can help you find the right options to get back on track. Taking action now can make a big difference in keeping your credit score healthy.

Final Thoughts: 7 Surprising Credit Score Myths That Are Hurting Your Financial Security Right Now

Understanding your credit score can be empowering, helping you make smart financial choices with confidence.

Every small step you take to understand and manage your credit better is a step toward financial freedom. Embrace the process, and trust that you’re making decisions today that will lead to a more secure and brighter financial future.

Don’t forget to come back and let me know how it goes!

A: No, checking your credit score won’t hurt it at all—it’s what’s known as a ‘soft inquiry,’ and it has zero impact on your credit. So, you can check your score as often as you like without worrying. The only time you might see a small dip is with ‘hard inquiries,’ which happen when you apply for things like credit cards or loans.

Q: Will carrying a balance on my credit card improve my credit score?

A: No, carrying a balance on your credit card won’t boost your credit score—in fact, it can do the opposite. When you carry a balance, it raises your credit utilization ratio, which is just a fancy way of saying how much of your available credit you’re using. The higher that percentage, the more it can hurt your score. It’s much better to pay off your balances in full each month to keep your utilization low and your credit score in good shape

Q. Does my income affect my credit score?

A: our income doesn’t directly affect your credit score. Instead, your score is determined by things like how well you pay your bills, how much of your available credit you’re using, how long you’ve had credit, and the variety of credit types you have. While having a higher income might make it easier for you to get higher credit limits, it does not directly affect your credit score.

Q: Should I close old credit cards to improve my credit score?

A: Not always. Since it appears as though you’re using more of your credit limit, it can actually lower your total available credit, which lowers your credit score. It can also reduce the length of time your credit history has been open. It is preferable to keep the card open and use it occasionally for modest purchases.

Q: Will paying off a loan always increase my credit score?

A: Paying off a loan can have mixed effects on your credit score. While it’s great for your overall financial health, closing a paid-off loan can temporarily lower your score by reducing your credit mix and potentially shortening your credit history. Focus on paying off high-interest debts while maintaining other accounts.

Q: Can my employer see my credit score when I apply for a job?

A: No, employers cannot see your credit score. They can view a simplified version of your credit report, which includes information about your debt and payment history. Plus, they need your permission first—employers must obtain your written consent before checking your credit report during the hiring process.

Q: Do student loans affect my credit score?

A: Yes, student loans do affect your credit score. Paying them on time can actually boost your credit by building a positive payment history. But if you miss payments or fall behind, it can seriously hurt your score. To stay on top of things, consider setting up autopay or looking into different repayment plans that make it easier to manage your payments.

Q: How does FICO 10 affect my credit score?

A: FICO 10 uses “trended data,” which means it looks at your credit behavior over time rather than just a snapshot. This model may penalize you for carrying high balances even if you pay them down slowly, making it even more important to keep your credit utilization low.

Q: Is using a debit card helpful for building my credit score?

A: No, using a debit card does not help build your credit score because debit card activity is not reported to credit bureaus. Only credit accounts, such as credit cards and loans, contribute to your credit history.

Q: When might it be a good idea to close a credit card?

A: It could be beneficial to close a credit card if it has high annual fees that outweigh the benefits, or if keeping the card open leads to overspending. However, consider downgrading to a no-fee card first to avoid affecting your credit history.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.